Identifying long-term Return On Investment (ROI) through the use of life-cycle cost analysis is nothing new. The use of ever-more-sophisticated software programs to crunch the numbers has introduced an admirable exactitude to life-cycle cost analysis. However, since it is the purveyor of the solution rather than the user of the analysis who establishes the ROI tool’s parameters and premises, some healthy skepticism is in order.

Even if the data plugged in is 100 percent accurate, it is still the seller who is writing the rules of the game. By establishing an erroneous or misleading set of parameters, the purveyor can deliberately tip the results in his favor. Requesting a third party to audit a manufacturer’s ROI claims is one way to resolve this problem. Meanwhile, these resources will give you the information you need to ask the right questions of your suppliers, so that you can critically analyze life-cycle performance claims.

You cannot achieve an accurate comparison of roofing costs without a realistic assessment of what the cost of each system will be. Obtaining actual quotes based on the specific parameters of your roofing project is the best way to start. Since installation costs will vary greatly according to the system being installed, the costs used for analysis should be installed costs based on actual quotes from the same contractor, whether you are comparing material solutions from one or several manufacturers.

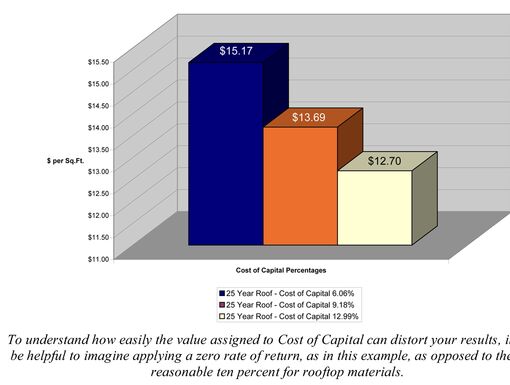

Simply put, the life-cycle costs of materials that last longer, but have a higher initial cost, will look better when you use a higher inflation rate. Conversely, a manufacturer selling only single- ply solutions will want to use an inflation rate as low as possible to keep down the costs of future replacements. Since typically you are going to be comparing the solutions of multiple manufacturers, it’s important to have an open discussion about the rate of inflation used by the ROI tool.

Although three percent is typical of the inflation rate used by the Consumer Price Index (CPI) during a stable economy, this rate varies greatly by industry, and as economies cycle through through periods of recessions and growth. The recent and anticipated volatility of oil and asphalt prices could justify an inflation rate for roofing as high as 12 percent.

When applying the inflation rate, it’s also important that the life-cycle costing tool allow you to differentiate the rate used for materials from the rate used for labor, as the expectations for each will vary greatly. For example, the anticipated inflation rate for materials might be seven percent while the anticipated inflation rate for labor might be only four-and-one-half percent. A good representation for a typical roofing project would be 40 percent of the costs for roofing materials using the higher inflation rate, and 60 percent of the costs for the labor portion using the lower inflation rate.

Ideally, the ROI tool used will allow you to assign realistic inflation rates to both materials and labor. In any case, it is important that you understand the rate(s) of inflation used by the tool, and the rationale on which it is based, so that you can fairly compare one manufacturer’s system against another’s.

Don’t cut corners when you are contributing your own estimates to the calculations performed. For example, even if your salaried in-house maintenance team will be handling all maintenance and repairs except for major restorations and replacements, you still need to make sure that the internal costs of maintenance are approximated based on the anticipated hours per year, with your own labor costs adjusted for inflation, in order to create an apples-to-apples comparison of costs. And though it sounds obvious, double-checking the calculations is always sound practice, as is giving the results a reality check based on your own facility maintenance management experience. If a result looks too good to be true, it probably is.

A good ROI tool will display the following parameters so that an independent audit can be made: